Knowledge Base

What categories are you using for bookkeeping?

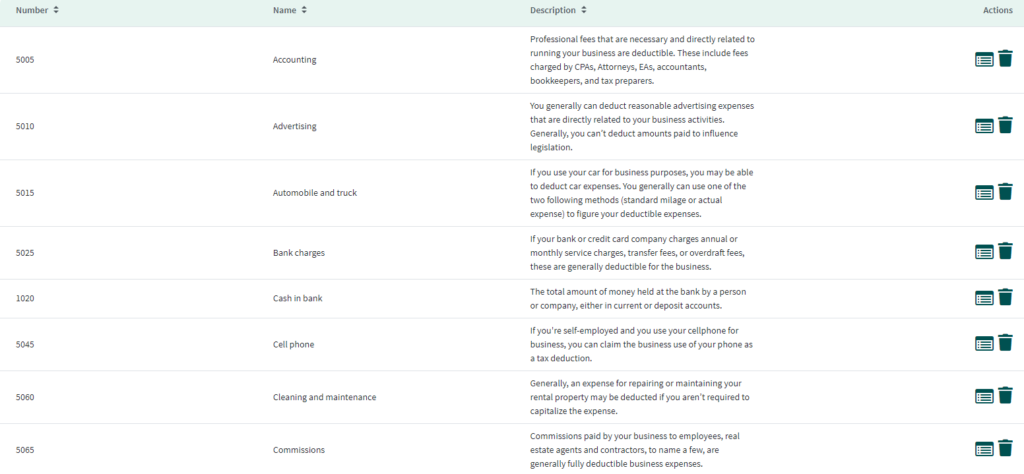

Overview of Base Accounts in Hedgi

Base accounts are the fundamental building blocks of your chart of accounts in Hedgi:

- Include major balance sheet categories like cash, accounts receivable/payable, inventory, fixed assets, and equity.

- Also cover main income statement categories like revenue, cost of goods sold, operating expenses.

- Have assigned account numbers starting with 1000s to indicate their foundational role.

- Provide the core framework for tracking broader financials.

- Can be further subdivided into more specific sub-accounts as needed.

- Are considered standard accounts that most businesses will utilize.

While base accounts establish a solid accounting foundation, Hedgi allows easily creating customized sub-accounts tailored to your business’s specific needs and organizational structure.

Leverage Hedgi’s preset base accounts to simplify getting started. Build on them with your own granular accounts for specialized tracking and reporting.